The introduction of Maastricht criteria that stipulated fiscal prudence by obliging EU member states to adhere to the level of public debt below 60 percent of the GDP and low fiscal deficit boosted the expectations of stable macroeconomic environment, partly sustained by the European Central Bank which, since its inception in 1999, successfully maintained price stability. Despite an enviable achievement in the stabilization of inflation expectations, the EU Treaty did not stipulate stringent fiscal rules in case of the breach of treaty obligations on behalf of EU member states, neither has European Growth and Stability Pact (EGSP) provided selective mechanisms that would hinge on the EU member state in case Maastricht criteria were not fulfilled. On the other hand, the gradual enlargement of the European union did not finalize in the economic union characterized by the realization of four basic freedoms.

In 1977, Portugal and Spain were acceded into the European Union. Four years late, Greece was admitted as the 12th member of the European community. Over time, the EU grew from an integrated area of 15 Western European countries into a conglomerate of nations that did not impinge of the full-fledged liberalization of the internal market in 1988 but, moreover, has evolved into the spiral that accelerated the community toward the political union. In the mean time, member states of the Eurozone have continuously breached the rules laid out by Maastricht treaty. In bearing the fiscal consequences of the reunification, Germany repeatedly breached the Maastricht criteria both in public debt and fiscal deficit which postponed the introduction of the Euro, following a large shock from gigantic fiscal transfers from high-income West Germany into low-income East German regions. In a similar manner, until 2005, France did not manage to reduce the debt-to-GDP ratio under the 60 percent threshold stipulated by the Maastricht criteria.

Nevertheless, peripheral countries such as Spain and Portugal entered the Eurozone at an overvalued exchange rate relative to German mark before the introduction of the common currency. In the following years, these countries, notably Spain, accumulated significant current account surpluses resulted from the inflows of direct investment from the core countries such as Germany and France. These surpluses were, of course, artificial in the sense that the downward convergence of interest rates in the peripheral countries stimulated the over-leveraging of the financial sector which triggered a balloon in the housing sector.

For years, Italy and Greece have repeatedly breached the Maastricht treaty in the fiscal sense. Prior to adjoining the European Monetary Union, Greece repeatedly experienced volatile inflation rates and default on its external obligations and subsequent Drachma depreciation. Italy’s macroeconomic stabilization hinged on the discretion of government spending which, after excessive rises under various transition governments, cumulated in one of the highest debt ratios within the EMU. How could EMU countries, despite a stringent set of rules delineated by the Treaty of Maastricht, pursued discretionary fiscal policies and jeopardized the macroeconomic stability of the national economies and the Eurozone?

For years, Italy and Greece have repeatedly breached the Maastricht treaty in the fiscal sense. Prior to adjoining the European Monetary Union, Greece repeatedly experienced volatile inflation rates and default on its external obligations and subsequent Drachma depreciation. Italy’s macroeconomic stabilization hinged on the discretion of government spending which, after excessive rises under various transition governments, cumulated in one of the highest debt ratios within the EMU. How could EMU countries, despite a stringent set of rules delineated by the Treaty of Maastricht, pursued discretionary fiscal policies and jeopardized the macroeconomic stability of the national economies and the Eurozone?

Prior to the onset of the financial crisis by the end of 2007, little was known on the perils of excessively leveraged balance sheets which investment banks used to seek high rates of return on high-yield and relatively risky peripheral regions. Until 2007, the exposure of major German investment to over-leveraged financial sector in countries such as Spain and Greece generated sizeable spillover effect. Before the onset of the financial crisis, Spain enjoyed sizeable current account deficit resulted from excessively high and robust overall investment. In 2007, Spain’s investment-to-GDP ratio (31 percent) was roughly comparable to developing Asia. In such highly volatile environment where economic growth departed from its long-run fundamentals, even small-scale macroeconomic shocks can result in a substantial loss of economic activity, notwithstanding the spillovers in the banking system and labor market.

The asymmetry in political structures and underlying macroeconomic fundamentals across member countries casts significant doubt in the long-term stability of the Eurozone as an area with common monetary policy. The necessary condition for the inception of common monetary policy does not hinge on the political initiatives that pervaded the process of European integration but on the careful consideration whether adjoining countries adhere to the macroeconomic criteria as denoted by the Maastricht Treaty. The failure to adhere to the contours of fiscal prudence and budgetary discipline by the major EU member states, with few notable exceptions such as the Netherlands, Austria and Finland, lies at heart of the underlying reasons why significant asymmetry and non-coordination in fiscal policy resulted in the adoption of dispersed economic policies whereas the adverse outcomes were not foreseen neither by the politicians neither by policy advisers and academics.

The asymmetry in political structures and underlying macroeconomic fundamentals across member countries casts significant doubt in the long-term stability of the Eurozone as an area with common monetary policy. The necessary condition for the inception of common monetary policy does not hinge on the political initiatives that pervaded the process of European integration but on the careful consideration whether adjoining countries adhere to the macroeconomic criteria as denoted by the Maastricht Treaty. The failure to adhere to the contours of fiscal prudence and budgetary discipline by the major EU member states, with few notable exceptions such as the Netherlands, Austria and Finland, lies at heart of the underlying reasons why significant asymmetry and non-coordination in fiscal policy resulted in the adoption of dispersed economic policies whereas the adverse outcomes were not foreseen neither by the politicians neither by policy advisers and academics.

To a large extent, as the recent debt crisis has succinctly demonstrated, the ultimate goal of the European monetary integration was the build-up of political union. But whereas European politicians were preoccupied with all-embracing design of the EU as unitary political union, they forgot to acknowledge that political union would require the full convergence of economic policies including the integration of the labor market which hardly any political initiative within the EU deemed feasible.

The non-coordination of fiscal policymakers was highly evident in the division of member states on the core countries and EU periphery. Considering the peripherical countries, Italy, Spain, Portugal and Greece repeatedly proved ill-disciplined in managing the levels of public debt and the magnitude of the budgetary imbalance. Portugal is often the case in point. Prior to the introduction of the Euro, Portugal experienced unprecedented economic boom. Between 1995 and 2001, economic growth averaged 4 percent per annum and the unemployment rate reduced from 7 percent to 4 percent by the end of 2001.

The non-coordination of fiscal policymakers was highly evident in the division of member states on the core countries and EU periphery. Considering the peripherical countries, Italy, Spain, Portugal and Greece repeatedly proved ill-disciplined in managing the levels of public debt and the magnitude of the budgetary imbalance. Portugal is often the case in point. Prior to the introduction of the Euro, Portugal experienced unprecedented economic boom. Between 1995 and 2001, economic growth averaged 4 percent per annum and the unemployment rate reduced from 7 percent to 4 percent by the end of 2001.

At the same time, nominal wages grew rapidly without the necessary productivity growth compensating for the increase unit labor cost. Alongside the overheating of economic activity, driven by construction boom, current account deficits increased significantly, lowering domestic savings rate. After the country experienced a mild recession in 2003 when domestic output decreased by 1 percent on the annual basis, the slowing of artificial economic growth driven by the Euro boom, turned from temporary into permanent. In the period 2002-2010, growth of domestic output averaged at the level of no more than 1 percent per annum with stagnating productivity and significant pressure on nominal wages. Since the size of the labor cost is the major deterrent on growth, the cure for Portuguese ailing economy is the structural adjustment in the public sector such as the reduction of public debt by generating substantial primary fiscal surpluses and the lowering of government spending. Similarly, the experience of Greece, Spain and Italy suggests the evolution of the same pattern evolving over time although Italy has been known as low-growing economy during the boom time.

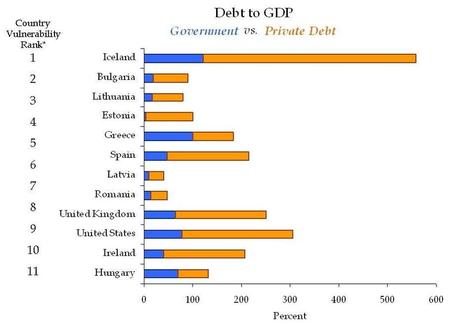

However, fiscal policymakers in peripheral countries repeatedly produced ill-conceived fiscal mismanagement of public finances. In 2008, the level of budgetary deficit in Greece exceeded 13 percent of the GDP whereas the country has not adhered to Maastricht criteria ever since the introduction of the Euro. After the depreciation, the net debt as percent of GDP in Greece reached 85 percent of GDP and increased to 110 percent of GDP by the end of 2008. As IMF’s recent forecasts suggest, by 2012, Greece’s public net debt could reach 175 percent of GDP.

However, fiscal policymakers in peripheral countries repeatedly produced ill-conceived fiscal mismanagement of public finances. In 2008, the level of budgetary deficit in Greece exceeded 13 percent of the GDP whereas the country has not adhered to Maastricht criteria ever since the introduction of the Euro. After the depreciation, the net debt as percent of GDP in Greece reached 85 percent of GDP and increased to 110 percent of GDP by the end of 2008. As IMF’s recent forecasts suggest, by 2012, Greece’s public net debt could reach 175 percent of GDP.

The failure to adhere to the common set of principles as delegated by the Maastricht treaty and EU Stability and Growth Pact in the peripheral countries stemmed largely from the mismanagement of public finances and structural rigidity of the public sector with resulting increases in the burden of the labor cost. In addition, the adoption of extraordinary measures embedded in the public sector such as very low effective retirement age and substantial bonuses for civil servants exacerbated the burden of the public debt with unforeseen net financial liabilities of governments which have not mitigated the persistent burden of public debt that grew substantially over time in the EU periphery.

A natural question is whether the exclusion of peripheral countries from the Eurozone might be feasible and whether Greece’s default on external obligations might help overcome country’s mountainous strain on public debt. First, the re-adoption of domestic currencies is hardly a solution to overcome the intricacies of debt crisis. If Greece re-introduced drachma, external obligations would be strained by a painful and enduring bank run since investors would withdraw the deposits from the portfolio and invest it into safer holding with less volatility and uncertainty ahead. Another argument in favor of Greece exiting the Eurozone is that a devaluation of drachma would boost inflationary expectations and consequently reduce the burden of the public debt but given junk score on government bonds, a rather immediate bank run would follow the devaluation of drachma rather than macroeconomic stabilization.

A natural question is whether the exclusion of peripheral countries from the Eurozone might be feasible and whether Greece’s default on external obligations might help overcome country’s mountainous strain on public debt. First, the re-adoption of domestic currencies is hardly a solution to overcome the intricacies of debt crisis. If Greece re-introduced drachma, external obligations would be strained by a painful and enduring bank run since investors would withdraw the deposits from the portfolio and invest it into safer holding with less volatility and uncertainty ahead. Another argument in favor of Greece exiting the Eurozone is that a devaluation of drachma would boost inflationary expectations and consequently reduce the burden of the public debt but given junk score on government bonds, a rather immediate bank run would follow the devaluation of drachma rather than macroeconomic stabilization.

In addition, when Greece’s domestic output is growing far below the long-term potential, inflationary expectations is not a feasible tool to revive the economy from deflationary trap with 16 percent unemployment Moreover, the only feasible and meaningful short-term strategy to boost growth is the reduction of the size of the public sector including the privatization of inefficient state-owned enterprises to generate substantial fiscal surpluses since this is the only plausible measure to tackle the increasing burden of the public debt. As the history of financial crises suggests, the eruptions of banking crises occurred mostly when governments rested on currency devaluations as the ultimate tool to reduce the burden of external debt. In addition, if Greece defaulted on its external obligations, CDS spreads could indicate a snowball effect where Spain, Portugal and possibly Italy could follow the same track.

The question is whether non-coordination between European fiscal policies helped facilitate over-leveraged financial sectors which asked for the bailout by central governments in the wake of the 2008/2009 financial crisis. Over-leveraged financial sectors were attributed to the determinants of various extent. Some argued that over-leveraging is the outcome of innovative financial engineering where fancy mathematicians and physicists applied VaR models to calculate the probability of losses in the portfolio distribution of returns whereas the financial derivative schemes developed by advanced and complex mathematical models were so complicated that nobody, sometimes even mathematicians themselves, could understand sensibly.

The question is whether non-coordination between European fiscal policies helped facilitate over-leveraged financial sectors which asked for the bailout by central governments in the wake of the 2008/2009 financial crisis. Over-leveraged financial sectors were attributed to the determinants of various extent. Some argued that over-leveraging is the outcome of innovative financial engineering where fancy mathematicians and physicists applied VaR models to calculate the probability of losses in the portfolio distribution of returns whereas the financial derivative schemes developed by advanced and complex mathematical models were so complicated that nobody, sometimes even mathematicians themselves, could understand sensibly.

On the other hand, the monetary policy perspective of over-leveraged financial sectors has been rather overlooked in policy discussions since periodically low interest rates encourage excessive risk-taking which further facilitated the construction of portfolios with excessively volatile returns that increasingly relied on VaR assumptions whilst fundamentally ignoring the instability of returns from over-leveraged investments. But a more intriguing question pertaining to the banking perspective of financial crises is whether more prudent financial regulation as envisaged from recent stress tests by European Banking Authority can be achieved by raising capital adequacy standards. Unfortunately, the history of Basel accords demonstrates that the banking sector has been prone to search alternative channels to avoid raising capital adequacy ratios through innovative accounting tricks whereas neither Basel I and II envisaged the adverse outcomes from excessive risk-taking. As stress tests indicated, capital adequacy ratios should be increased substantially but, moreover, the regulatory framework should not only build on increasing criteria on Tier I capital and common equity but also on the safeguard despositary insurance of contingent liabilities to mitigate liquidity risk that led to the systemic crisis.

The solution to revive the Eurozone economy and revive it from a decade of flawed political imperatives should not exclude multiple options. The focal point of the Eurozone’s recovery from debt crisis should be to help peripheral countries establishment fiscal prudence, discipline and soundness of the public finances. In fact, the recovery from the debt crisis will endure for more than a decade. The structural adjustment does not rest on the ability of the EU to provide financial assistance to peripheral countries but on the principled and coordinated action to reform inefficient public sectors which are at the heart of the debt spiral since years of generous entitlements to civil servants have tremendously raised the net present value of public debt to the point that peripheral countries are on the brink of default on its external obligations. Without generating substantial fiscal surpluses, there is no feasibility and no realistic scenario under which public debt level would be brought under the control in the near-term perspective. Hence, recent discussions of the consequences of debt crisis in Europe have simply overlooked the importance of growth-enhancing measures as the real cure for growing debt-to-GDP ratio where the measures do not apply to peripheral countries only.

First, in the wake of fiscal insolvency of public pension systems, effective retirement age should be raised substantially for men and women alike. The studies have shown that under the increase in effective retirement age to 65 years, long-term fiscal obligations would reduce and consequently an important step towards long-term macroeconomic stability would be achieved. Nearly every European country is facing low-fertility trap followed from increased affluence and generous early-retirement policies from 1970s onward. Consequently, European government have amounted a mountain of net financial liabilities that exceeded the size of GDP by several times, respectively. Decreasing the size of net liabilities to contemporary and future generations of retirees, requires a robust increase in effective retirement age. Higher retirement age threshold would substantially increase working-age population by encouraging labor market participation among the elderly. Current levels of effective retirement age are unsustainable in the long-run since a growing burden of pension obligations can seriously threaten the stability of the public finance and increase the probability of fiscal insolvency.

Second, European countries suffer from low productivity growth. In some countries, such as Italy productivity growth has remained stagnant over the course of recent two decades while elsewhere productivity growth is to slow to compensate for the increase in nominal wage rates. The evidence, in fact, overwhelmingly suggested that high tax rates are the prime obstacle to greater labor market participation, particularly among the elderly who face high implicit tax rates on work. In particular, to facilitate the channels of productivity growth, marginal tax rates should be decreased substantially. At current levels, marginal tax rates restrain labor supply significantly. In the Netherlands, the top marginal income tax rates reached 52 percent in 2011 which is a serious hinder on the working activity. In this respect, bold tax reforms should be complemented with more flexible labor markets which remain saddled with employment regulations and distort labor supply incentives. Less regulated labor market to supplement greater labor force participation, especially among women, elderly and the youth is vital to enhance productivity growth since living standards by the end of the day are determined by productivity improvements.

Ultimately and most importantly, peripheral countries should be given a free choice whether to withdraw from the EMU since recent financial crisis has shown that Eurozone is a suboptimal currency area which emerged from non-cooperative fiscal policies among its member states that caused adverse outcomes and asymmetric adjustment where macroeconomic stabilization outcomes are mutually exclusive among member states. Asymmetry adjustment that currently threatens the existence and stability of Eurozone lies at the heart of Eurozone’s debt crisis. As a general matter, economic policies have failed to recognize that structural measures in the labor market and fiscal policy regime could facilitate growth enhancement and provide the necessary impetus to stabilization of crisis-impeded monetary union. Recent suggestions by France and Germany for EU member states to form a fiscal union have led to sustained resistance from the UK which dissolved from the fiscal pact.

The solution to revive the Eurozone economy and revive it from a decade of flawed political imperatives should not exclude multiple options. The focal point of the Eurozone’s recovery from debt crisis should be to help peripheral countries establishment fiscal prudence, discipline and soundness of the public finances. In fact, the recovery from the debt crisis will endure for more than a decade. The structural adjustment does not rest on the ability of the EU to provide financial assistance to peripheral countries but on the principled and coordinated action to reform inefficient public sectors which are at the heart of the debt spiral since years of generous entitlements to civil servants have tremendously raised the net present value of public debt to the point that peripheral countries are on the brink of default on its external obligations. Without generating substantial fiscal surpluses, there is no feasibility and no realistic scenario under which public debt level would be brought under the control in the near-term perspective. Hence, recent discussions of the consequences of debt crisis in Europe have simply overlooked the importance of growth-enhancing measures as the real cure for growing debt-to-GDP ratio where the measures do not apply to peripheral countries only.

First, in the wake of fiscal insolvency of public pension systems, effective retirement age should be raised substantially for men and women alike. The studies have shown that under the increase in effective retirement age to 65 years, long-term fiscal obligations would reduce and consequently an important step towards long-term macroeconomic stability would be achieved. Nearly every European country is facing low-fertility trap followed from increased affluence and generous early-retirement policies from 1970s onward. Consequently, European government have amounted a mountain of net financial liabilities that exceeded the size of GDP by several times, respectively. Decreasing the size of net liabilities to contemporary and future generations of retirees, requires a robust increase in effective retirement age. Higher retirement age threshold would substantially increase working-age population by encouraging labor market participation among the elderly. Current levels of effective retirement age are unsustainable in the long-run since a growing burden of pension obligations can seriously threaten the stability of the public finance and increase the probability of fiscal insolvency.

Second, European countries suffer from low productivity growth. In some countries, such as Italy productivity growth has remained stagnant over the course of recent two decades while elsewhere productivity growth is to slow to compensate for the increase in nominal wage rates. The evidence, in fact, overwhelmingly suggested that high tax rates are the prime obstacle to greater labor market participation, particularly among the elderly who face high implicit tax rates on work. In particular, to facilitate the channels of productivity growth, marginal tax rates should be decreased substantially. At current levels, marginal tax rates restrain labor supply significantly. In the Netherlands, the top marginal income tax rates reached 52 percent in 2011 which is a serious hinder on the working activity. In this respect, bold tax reforms should be complemented with more flexible labor markets which remain saddled with employment regulations and distort labor supply incentives. Less regulated labor market to supplement greater labor force participation, especially among women, elderly and the youth is vital to enhance productivity growth since living standards by the end of the day are determined by productivity improvements.

Ultimately and most importantly, peripheral countries should be given a free choice whether to withdraw from the EMU since recent financial crisis has shown that Eurozone is a suboptimal currency area which emerged from non-cooperative fiscal policies among its member states that caused adverse outcomes and asymmetric adjustment where macroeconomic stabilization outcomes are mutually exclusive among member states. Asymmetry adjustment that currently threatens the existence and stability of Eurozone lies at the heart of Eurozone’s debt crisis. As a general matter, economic policies have failed to recognize that structural measures in the labor market and fiscal policy regime could facilitate growth enhancement and provide the necessary impetus to stabilization of crisis-impeded monetary union. Recent suggestions by France and Germany for EU member states to form a fiscal union have led to sustained resistance from the UK which dissolved from the fiscal pact.

The ultimate grain of truth in the fiscal union is that a monetary union necessarily requires the coordination of fiscal policies to prevent adverse and asymmetric policy outcomes within the union. The fateful conclusion from recent EU debt crisis is that without the integration of the labor market on the EU level, the monetary integration cannot exist in coherence with asymmetric fiscal policies. In the future, stricter adherence to budgetary discipline will be necessary through budgetary authority. In this respect, countries that fail to adhere to Maastricht criteria and deviate from the fiscal discipline either marginally or substantially should be condemned and pay for their actions of fiscal imprudence by withdrawing from the monetary union.

{kind=link}